All Categories

Featured

Table of Contents

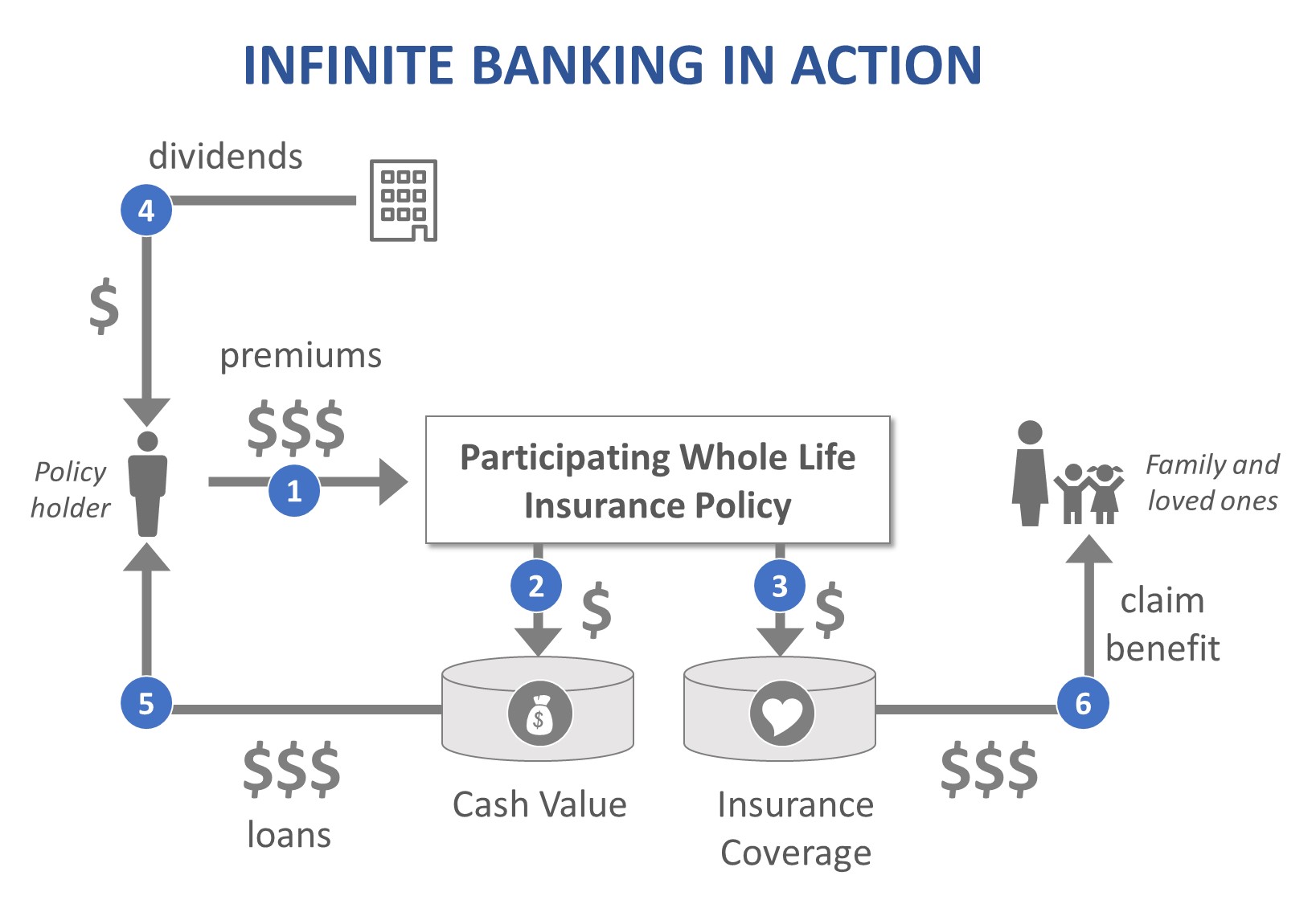

A PUAR permits you to "overfund" your insurance plan right up to line of it coming to be a Customized Endowment Agreement (MEC). When you utilize a PUAR, you rapidly raise your money worth (and your survivor benefit), thus enhancing the power of your "financial institution". Even more, the even more money worth you have, the higher your interest and dividend payments from your insurer will certainly be.

With the increase of TikTok as an information-sharing platform, monetary guidance and approaches have found an unique method of dispersing. One such method that has actually been making the rounds is the infinite banking principle, or IBC for brief, amassing recommendations from stars like rap artist Waka Flocka Flame. While the approach is currently popular, its roots trace back to the 1980s when economist Nelson Nash presented it to the world.

Can I use Self-financing With Life Insurance to fund large purchases?

Within these policies, the cash value expands based upon a price set by the insurance firm (Borrowing against cash value). As soon as a significant cash worth collects, insurance holders can acquire a cash money worth funding. These finances differ from conventional ones, with life insurance policy acting as security, implying one could lose their protection if borrowing exceedingly without appropriate money value to support the insurance prices

And while the attraction of these policies is noticeable, there are natural restrictions and risks, demanding thorough cash money value surveillance. The approach's authenticity isn't black and white. For high-net-worth individuals or company owner, particularly those using techniques like company-owned life insurance policy (COLI), the benefits of tax obligation breaks and substance development might be appealing.

The attraction of boundless financial does not negate its challenges: Cost: The fundamental demand, an irreversible life insurance policy policy, is costlier than its term equivalents. Qualification: Not every person gets approved for entire life insurance policy due to strenuous underwriting processes that can leave out those with certain wellness or way of living problems. Complexity and risk: The complex nature of IBC, combined with its threats, might hinder several, specifically when simpler and less dangerous choices are available.

What financial goals can I achieve with Infinite Banking Account Setup?

Assigning around 10% of your month-to-month earnings to the plan is just not feasible for a lot of people. Using life insurance policy as a financial investment and liquidity resource requires technique and surveillance of policy cash worth. Consult a financial consultant to figure out if unlimited financial lines up with your concerns. Part of what you check out below is simply a reiteration of what has actually already been said over.

So before you obtain on your own right into a situation you're not planned for, recognize the complying with first: Although the principle is commonly marketed thus, you're not really taking a financing from yourself. If that held true, you wouldn't need to repay it. Instead, you're borrowing from the insurance company and have to repay it with rate of interest.

Some social media blog posts recommend utilizing cash worth from entire life insurance policy to pay down credit score card debt. When you pay back the lending, a section of that passion goes to the insurance coverage firm.

For the initial several years, you'll be paying off the commission. This makes it exceptionally difficult for your policy to build up value throughout this time. Unless you can afford to pay a few to a number of hundred bucks for the following decade or even more, IBC will not work for you.

What are the common mistakes people make with Leverage Life Insurance?

Not everyone needs to depend solely on themselves for financial security. If you need life insurance policy, here are some beneficial ideas to think about: Consider term life insurance policy. These plans offer protection throughout years with substantial financial responsibilities, like home loans, student lendings, or when caring for kids. See to it to search for the very best price.

Think of never ever needing to fret about financial institution financings or high rate of interest once again. What happens if you could obtain cash on your terms and construct riches at the same time? That's the power of unlimited banking life insurance coverage. By leveraging the money worth of entire life insurance policy IUL plans, you can expand your riches and borrow money without counting on typical financial institutions.

There's no set lending term, and you have the freedom to pick the settlement timetable, which can be as leisurely as settling the financing at the time of death. Cash value leveraging. This flexibility encompasses the servicing of the finances, where you can select interest-only payments, keeping the financing balance flat and convenient

Holding cash in an IUL repaired account being credited rate of interest can typically be much better than holding the money on down payment at a bank.: You've always fantasized of opening your very own bakeshop. You can borrow from your IUL policy to cover the first expenses of renting out an area, buying tools, and working with personnel.

Can Self-banking System protect me in an economic downturn?

Individual fundings can be gotten from traditional financial institutions and credit rating unions. Right here are some bottom lines to take into consideration. Credit report cards can give a flexible means to borrow cash for very temporary periods. Nonetheless, borrowing money on a charge card is typically very pricey with interest rate of passion (APR) often reaching 20% to 30% or even more a year - Infinite wealth strategy.

{kind=link}

Latest Posts

How To Become Your Own Bank And Build Wealth With ...

Bank On Whole Life

Infinite Banking Toolkit